(Idea) Calumet - Big Upside If The Market Prices The RIN Windfall

Previous write-ups on Calumet:

(Idea) Calumet Shares Sell Off Despite A Brightening Outlook

(Idea) Calumet - The Next Special Situation Idea

(Idea) An Important Update On Calumet

By: Jon Costello

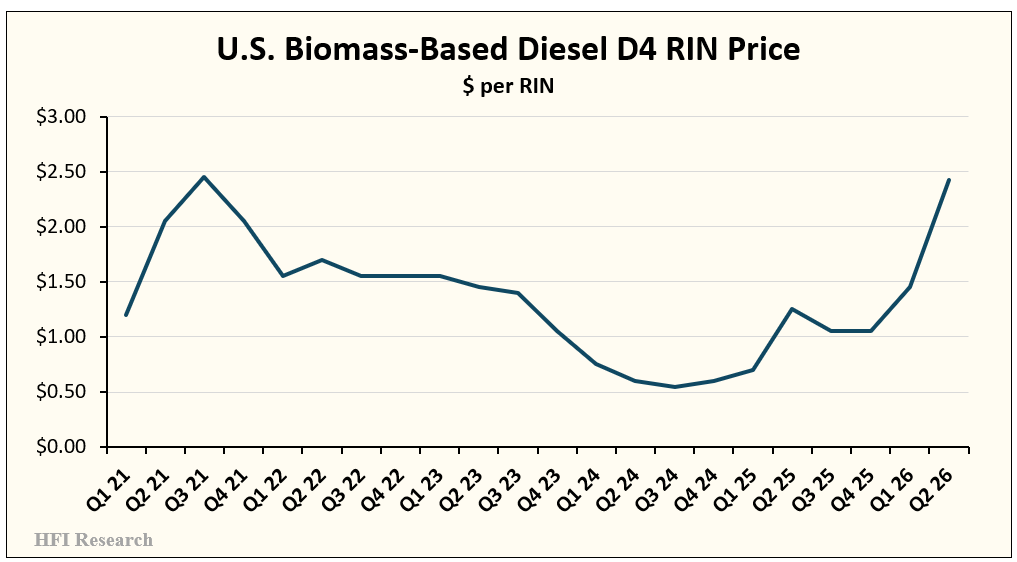

The price of biofuel compliance credits has doubled this year. For Calumet CLMT 0.00%↑ , the D4 RIN credit, upon which its Montana Renewables’ biofuel economics depend, traded at $2.42, just shy of its highest level since 2021. We have owned CLMT in our HFIR Energy Income Portfolio since June 2022, and in my May 20 article, I revised my valuation higher to approximately $50 per share as renewable diesel margins normalized.

CLMT shares are taking a hit, along with the broader energy sector, after the U.S. officially signed a memorandum of understanding with Iran to end hostilities. The shares currently trade around $31.75, back to where they traded when my previous article raised my valuation and well below my fair-value range, leaving the risk/reward unusually attractive relative to the upside potential in the shares.

This piece takes an unusual tack for my articles. It offers an ultra-bullish way to size the upside potential in CLMT shares. Specifically, it takes the cash CLMT’s renewable business will throw off in the back half of this year, assumes the market treats that windfall as permanent, and estimates where the stock might land in that scenario. To be clear, I don’t believe the windfall will be permanent. But the gap between what the RIN market is signaling and what CLMT equity now reflects is wide enough to be worth measuring.

Why RIN Prices Doubled: A Mandate the Industry Can’t Meet

First, it’s probably worth reviewing what a RIN actually is. “RIN” is short for Renewable Identification Number, a credit generated each time one gallon of biofuel is produced. The federal Renewable Fuel Standard requires that refiners and fuel importers blend a set volume of biofuel into the nation’s petroleum supply each year, and the required volume is called the Renewable Volume Obligation, or RVO. A refiner meets its obligation in one of two ways. It can blend the biofuel into its refined products itself, or it can buy the RIN credits from another party that did. When the federal RVO mandate is set above the level the industry can comfortably supply, refiners have to bid up RIN prices to pull every last gallon into the market.

Fortunately for CLMT and its peers that survived the brutal biofuel market over the past few years, the 2026 and 2027 mandates are the most aggressive in the program’s history, and the industry is nowhere near meeting them. In a June 10 analysis, agricultural economists Todd Hubbs and Scott Irwin estimated that required biomass-based diesel RIN generation must rise from 7.10 billion in 2025 to 10.99 billion in 2026 and 11.89 billion in 2027, which the researchers refer to as “levels that have no precedent in the history of the U.S. biomass-based diesel industry.” Actual output has been running well below the pace needed to hit the 2026 figure. The authors further state that closing the gap would require monthly production “more than 20 percent above the highest single month ever recorded,” sustained for the rest of the year. This is something the industry cannot do. So the RIN price should climb until demand is rationed.

Adding to the bullish picture is that the 45Z tax credit works against biofuel imports, thereby preventing a surge of foreign biofuels from substantially dampening the setup for domestic producers.

D4 RIN prices have already begun to surge, trading at $2.41 on June 18, near their 2021 record and 100% above their price at the start of this year. Because a gallon of renewable diesel—the biofuel produced by CLMT—generates 1.6 to 1.7 RINs, the EIA notes that these fuels “currently generate more than $3.50/gal of credits.”

The academic supply work, the EIA price series, and the futures market all indicate that a mandate the industry cannot physically meet is on course to trade to—and potentially exceed—its record price.

Moreover, risks to the RIN price outlook are easing. One such risk noted by the authors of the farmdoc article was that the oil price spike related to the Iran conflict could curb gasoline and diesel demand. Since the RVO sets the required biofuel volume as a fixed percentage of the petroleum gasoline and diesel supplied each year, a price spike that curbs fuel demand would shrink the obligated volume base to which the percentage applies, and with it, the volume of mandated biofuel blending and the demand for RINs. That risk has now receded with the United States and Iran introducing a framework to end the war and reopen the Strait of Hormuz. In response, WTI dropped by roughly one-third from its 2026 highs under $74 per barrel. With demand more likely to hold steady, the biofuel blending mandate will likely remain firm.

The U.S.-Iran deal helps on a second front, as well. A severe escalation would have driven refined-product prices high enough to crush end-user demand and destroy refining margins. Instead, with WTI prices easing and demand holding, the 2-1-1 crack spread is more likely to firm, a tailwind for asphalt production at Montana Renewables, which sits alongside the renewable plant.