(Idea) BP - Chronic Undperformer

Editor’s Note: Ideas from HFI Research is a separate paid subscription. BP is not a holding in the HFI Portfolio.

By: Jon Costello

We’re longtime followers of Elliott Management’s move in the energy space. The group has been outstanding at executing large-scale, control-type investments in public energy companies. It orchestrated a masterstroke with its business turnaround of Suncor Energy (SU). In that investment, Elliott spent many months analyzing and planning before accumulating its stake in the company. Its strategy was to install a new CEO, improve upstream operations, address worker safety challenges, and make the organization more efficient and shareholder-oriented.

By any measure, Elliott’s efforts have been a success. The most impressive part, in our view, is how rapidly the company was able to execute its planned improvements.

Elliott Buys a Stake in BP

On February 10, Elliott disclosed a nearly 5% stake in UK oil major BP PLC (BP).

Elliott is already profiting on the trade. Reports of Elliott’s stake sent the shares up more than 6%. Assuming Elliott purchased its stake in the fourth quarter in the $30 per share range, its nearly $5 billion stake is up more than 10% since they acquired it.

Source: Yahoo! Finance. Red text added by author.

Reports indicate that Elliott plans to reduce costs and dispose of assets to boost cash flow and achieve a leaner organization. The question for us is whether BP shares are a buy at their current price.

With all due respect to Elliott—and the near certainty that they have a sound understanding of the issues backed by a solid plan—we suspect BP will be a tougher nut to crack than Suncor. Until we can see what Elliott sees in BP, we plan to remain on the sidelines.

From our outside perspective, BP’s culture has driven underperformance for more than a decade. Cost cuts and asset disposals may boost profits in the near term. For one, BP is considering a sale of its Castrol lubricants business, which could fetch $10 billion—more than 10% of the company’s market cap. Sale proceeds could be put toward debt reduction, lowering BP’s interest expense and boosting free cash flow.

Looking longer term, however, we expect enhancing capital efficiency and improving returns on capital in a sustainable manner will be more difficult to achieve. This is why we’d rather avoid the name.

BP’s Antipathy for Hydrocarbons

BP competes for investors’ equity capital against its Western oil major peers. The company has underperformed these peers on important metrics for decades, causing it to lose out in the competition for capital. This is why its shares trade at a persistent discount.

BP’s low returns on capital stem from years of poor capital allocation. We believe an important source of BP’s persistent capital allocation underperformance is its cultural antipathy to its hydrocarbon operations.

BP’s attitude toward hydrocarbons goes back to the leadership of John Browne, who introduced BP’s tagline “Beyond Petroleum” shortly after becoming CEO in 2001. The move was an attempt to push public perception away from BP’s “British Petroleum” roots and toward non-hydrocarbon energy sources that Browne believed would drive the energy industry’s growth over the long term. The marketing makeover backfired spectacularly in 2010 after the Deepwater Horizon disaster, from which BP’s image never fully recovered.

Since Browne, BP hasn’t abandoned its antipathy toward hydrocarbons, which is palpable in its governance and communications with shareholders and the public.

At times, the company’s attitude toward hydrocarbons verges into aversion or even disdain. Its annual reports read as if it is ashamed that its bread-and-butter business revolves around producing, refining, marketing, and distributing crude oil, natural gas, and refined products.

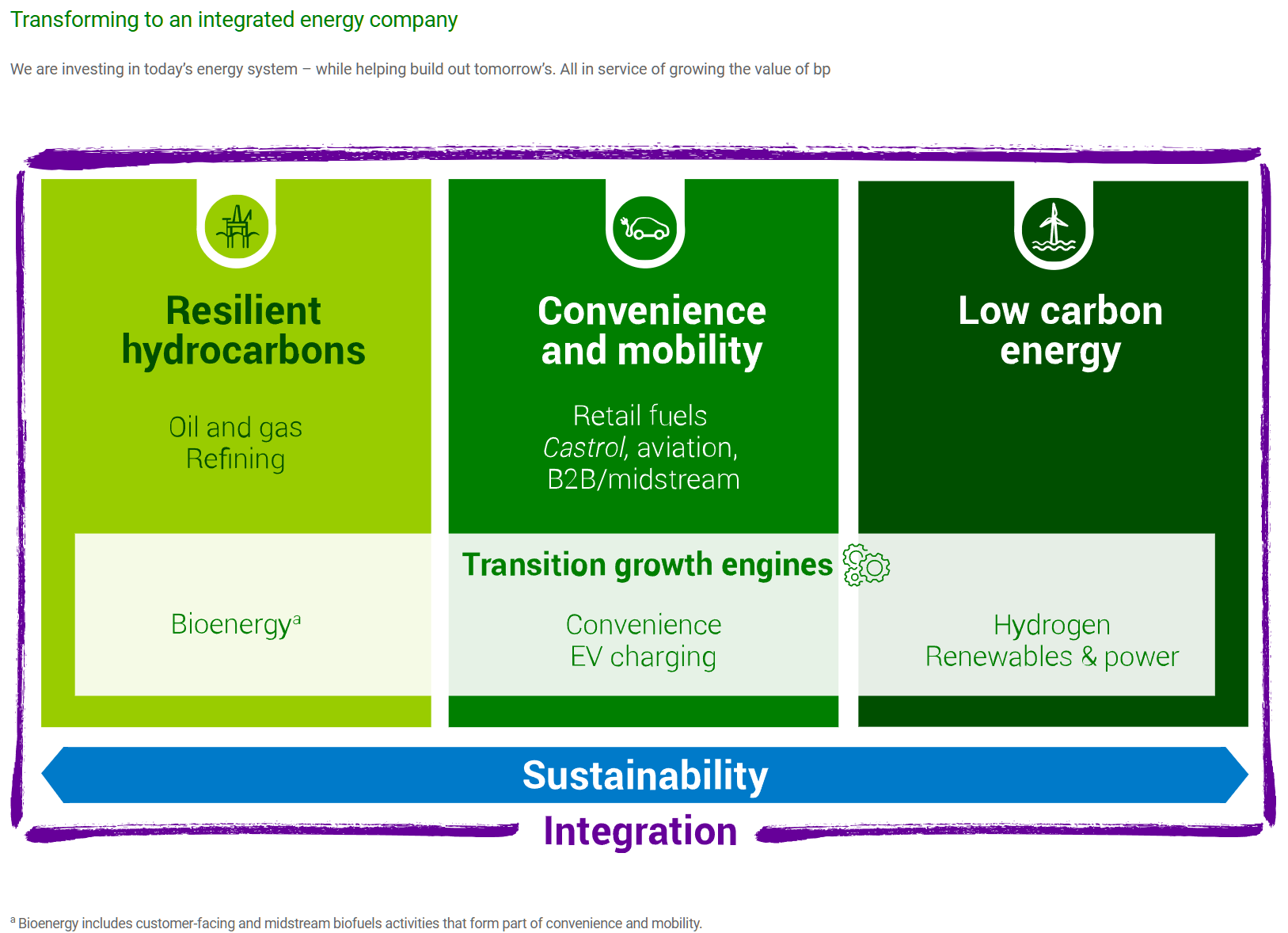

For instance, the title page of BP’s 2023 annual report states that it is changing “from an international oil company to an international energy company” as if to proclaim a break with its “dirty” past. On the first page of the report, readers are greeted by the following graphic, which is meant to depict the company’s strategy.

Source: BP 2023 Annual Report.

What is “resilient hydrocarbons” supposed to mean, anyway?

The report then delves into updates about:

Scope 1 and 2 emissions.

Building out a network of EV charging stations.

The methane intensity of BP’s oil production.

The company’s contributions toward net-zero emissions and meeting the Paris goals.

New low-carbon projects.

BP’s acquisition of Lightsource bp, an owner and operator of utility-scale solar and battery storage assets.

Fourteen pages of “Climate-related financial disclosures.”

As oil and gas company shareholders, these initiatives are very low on our priority list. Reading the report, it becomes clear that BP isn’t suffering from an identity crisis. It’s aware of its identity; it’s simply ashamed of it.

Elliott has been successful in changing company culture—witness the safety improvements and shareholder orientation it ushered in at Suncor. We’d argue BP needs a cultural shift toward embracing hydrocarbons. Such a change would make us more confident that the company can improve its returns. Change would have to start at the board. Bringing in a hard-charging, no-nonsense, returns-per-share-focused CEO like Elliott did at Suncor would also help.