(Idea) Baytex Energy - Selling Eagle Ford Was The Right Move Making It A More Attractive Oil Name

Note: This article cites Canadian dollars unless otherwise specified.

Baytex Energy (BTE) is transitioning from a 150,000 boe/d, 86% liquids producer with operations split 55%/45% between the U.S. and Canada to a Canadian pure play that will produce 65,000 boe/d and 91% liquids. In the process, BTE will shed its legacy as an uninvestible stock and emerge as a potentially attractive long-term holding.

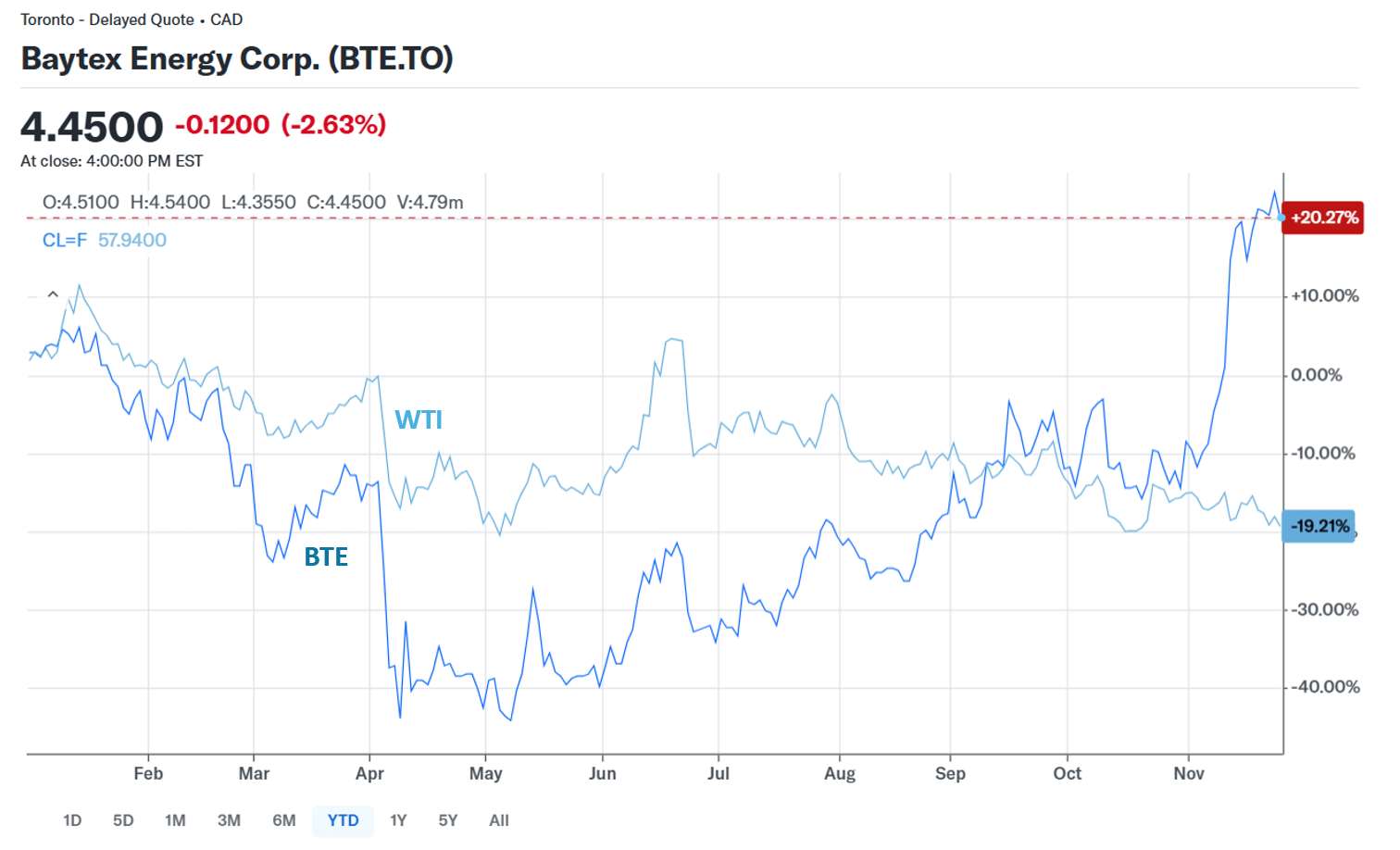

The market is pleased with the changes. BTE shares have surged 19% in response to the company’s November 12 announcement that it would dispose of its U.S. assets. The stock’s reaction to the deal accelerated its recent trend of outperformance versus WTI after a long stretch of underperformance.

Source: Yahoo! Finance, Nov. 25, 2025.

Recall that in 2022, before BTE acquired Eagle Ford operator Ranger Oil, it produced a total of 87,000 boe/d, of which 30,000 boe/d was from the Eagle Ford and 57,000 was from Canada. The Ranger acquisition brought an additional 68,000 boe/d of exclusively Eagle Ford production that was contiguous with BTE’s own acreage. In the recently announced transaction, BTE sold the entirety of its U.S. assets, which produced approximately 82,800 boe/d in the third quarter.

By disposing of its U.S. assets, BTE shareholders will trade 401 million barrels of U.S. reserves and 82,800 boe/d of production for $3.25 billion in cash and a smaller, but cleaner, net asset base. The company will use the cash proceeds to eliminate its long-term debt. Management is guiding to a net cash position of $900 million after the deal closes. The deal will reduce 2P NAV from $7.27 per share to $5.13, for a 29% decrease. However, eliminating debt will substantially de-risk the NAV of the smaller asset base. Going forward, BTE’s smaller Canadian asset base will grow at a materially faster rate than its former asset base over the coming years.

The deal highlights management’s subpar capital allocation abilities. The Eagle Ford asset excursion saw it behave in a grossly pro-cyclical manner, precisely the opposite of how commodity company capital should be allocated to best create long-term value. BTE acquired Ranger when WTI was trading in the high-US$70s. Now it’s disposing of the acreage with WTI in the mid-to-high US$50s. That said, management may have slightly redeemed itself on the natural gas side. BTE’s Eagle Ford acreage produced 18% natural gas. No doubt the gas exposure was attractive to the asset buyer, as gas has become the go-go asset in the energy space. So, for natural gas, one can argue that BTE behaved appropriately counter-cyclically.

Still, management should be congratulated for recognizing the blight that the Eagle Ford assets represented on BTE’s stock. The move is an implicit acknowledgement by management that it made a mistake in acquiring Ranger. It is effectively correcting its mistake through this sale.

Overall, I like the deal and what it means for long-term BTE shareholders. The next step is to determine whether they’re worth buying.