(Idea) Baytex Energy - More Negatives Than Positives

At the moment, Baytex Energy (BTE:CA) bears are winning the day. Year-to-date, the shares have struggled, gaining 5.5% versus the broader Canadian E&P Index (XEG:CA), which is up 22.5% over the same timeframe.

BTE is the ultimate battleground E&P stock because both the bulls and bears have valid arguments for the stock’s purported huge upside and downside cases. For the time being, however, we count ourselves in the bear camp until the company demonstrates it can address the factors that cloud its longer-term outlook and management executes on its capital return plan for several quarters.

BTE Bulls Have a Case

BTE shares are generally held for their upside amid higher oil prices. As oil prices climb, the company’s free cash flow surges higher at a rate that few of its peers can match.

At $80 per barrel WTI and $2.25 per MMBtu AECO, we estimate the company generates C$790 million of free cash flow, equivalent to C$0.96 per share and a 20.1% free cash flow yield on the current stock price of C$4.64. If the shares were to trade at a 12% free cash flow yield, they would trade at C$8.00, implying upside of 73%. This represents the tremendous upside potential in the shares using commodity assumptions that are hardly heroic.

Management intends to allocate the company’s free cash flow 50%/50% between debt repayment and a mix of dividends and share repurchases. Once net debt is reduced from C$2.6 billion to C$1.5 billion, the company intends to boost its payout to 75% of free cash flow.

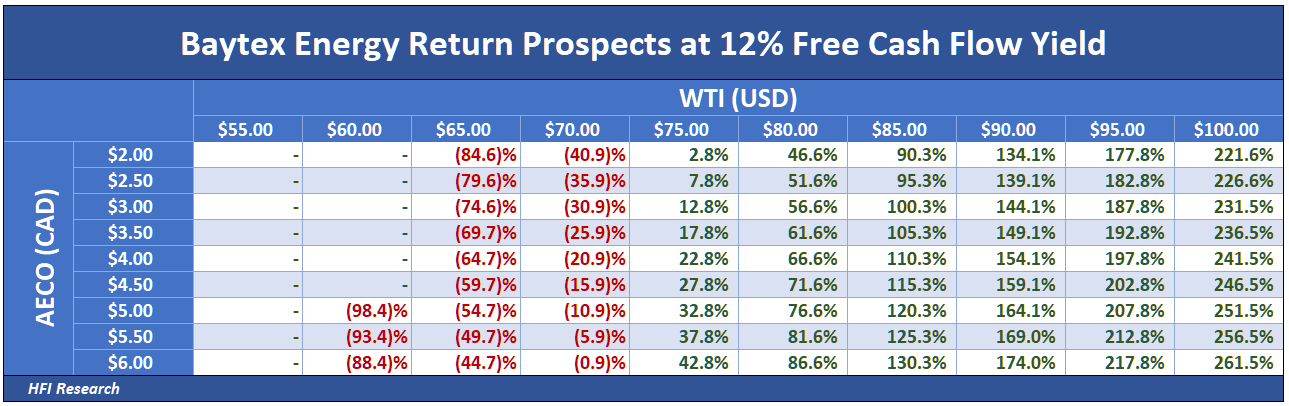

It’s worth taking a look at the upside in BTE shares at higher oil prices.

The table below demonstrates the company’s tremendous cash flow torque to commodity prices.

On a per-share basis, BTE’s free cash flow yield looks as follows.

And if the shares were to trade at a 12% free cash flow yield, their return profile at different commodity prices look like this:

While these are eye-popping returns, they improve materially if we factor in share repurchases. For example, assuming a flat $80 per barrel WTI and C$4.62 stock price, share repurchases from free cash flow after dividends over the next three quarters alone would eliminate 58.2 million shares. BTE’s share count would fall from 821.7 million at the end of the first quarter to 763.5 million at year-end. At that point, the share repurchases would have caused 2024 free cash flow per share to increase from C$0.96 to C$1.04 while the free cash flow yield on the current share price would rise from 20.86% to 22.4%—quite an improvement in only three quarters at $80 per barrel WTI.

At our assumed 2024 commodity prices of $87.50 per barrel WTI, $2.25 per MMBtu AECO, and a $13.50 per barrel WTI-WCS differential, free cash flow comes to C$1.09 billion, resulting in C$9.87 of value from a discounted cash flow perspective using a conservative 12% discount rate and cutting the terminal value in half. The implied return from the current stock price of C$4.62 is 114%.

BTE has other things going for it. Its first-quarter production results met analyst consensus expectations. Drilling results have been good, and the company recently expanded in the Duvernay. Management is touting Eagle Ford “refracs” on pre-2017 wells as achieving 100% IRRs, which could boost cash flow torque further.

Net debt stood at C$2.64 billion at the end of the first quarter, though it was inflated by a weak Canadian dollar. Debt is approximately 1.3-times funds from operations at $80 per barrel WTI, on the high side for an E&P these days but not concerning in light of our positive outlook for oil prices over the coming years. The company also recently executed a private offering of C$575 million of 7.375% senior unsecured notes to redeem its 8.75% notes due 2027 and push the maturity out to 2028.

These positives are why BTE shares are among the go-to names for investors who expect higher oil prices. Based on cash flow growth alone, they offer the prospect of more than a double with WTI sustained at $80 per barrel and AECO at $3.00 per MMBtu.