(Idea) AdvanSix - Lowest Cost Producer, Trading At Half Of Book Value, And Cycle Trough

By: Jon Costello

AdvanSix (ASIX) was spun off from Honeywell (HON) on October 1, 2016, to create a company that could focus on pursuing its unique growth strategy. ASIX occupies a low-cost position in several niche chemical products. The company’s products face an oversupply and weak demand, which is removing capacity. Prices are currently unsustainable, and ASIX is positioned to thrive once conditions improve.

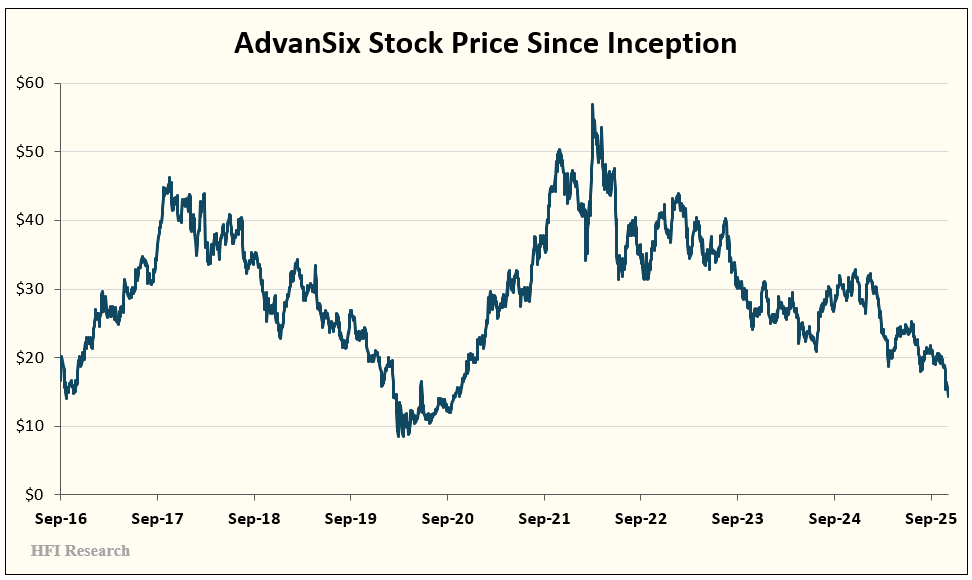

The stock has trended lower since hitting its last cyclical peak in 2022.

Stocks like ASIX generate the highest returns when they’re bought at cyclical lows, when industry conditions and investor sentiment are in the dumps. That’s where ASIX is today, which makes its stock an attractive long-term buy.

ASIX Overview

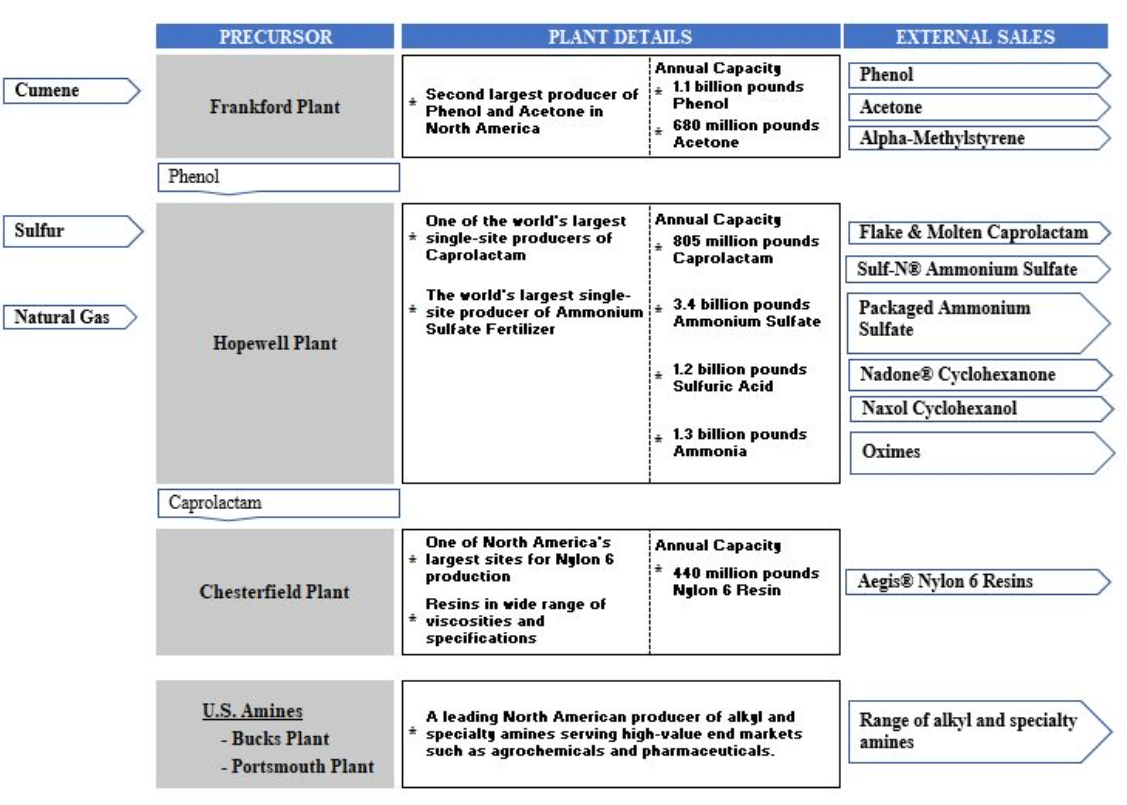

ASIX operates an integrated chemical manufacturing chain with five production sites across the U.S. The company converts cumene, ammonia, sulfur, and other feedstocks into nylon 6 resin, caprolactam, ammonium sulfate, and various phenol and acetone-based intermediates. Through its vertical integration, it captures value at each step of the production chain, lowering unit costs and improving margins.

Nylon 6 & Caprolactam

Nylon 6 and caprolactam account for approximately 41% of ASIX’s revenue. The split is 23%/18% between nylon and caprolactam. Plant nutrients account for 30% of revenue, while various chemical intermediates account for the remaining 29%.

Approximately 90% of ASIX’s sales take place in the U.S. Its customers operate across U.S. industry in construction, fertilizer, agrochemicals, plastics, solvents, packaging, adhesives, and electronics. Its U.S.-centered operations provide an additional competitive advantage from lower transportation costs and logistical advantages relative to global competitors selling in the U.S. ASIX’s U.S. weighting renders it exempt from the reciprocal tariffs that have negatively impacted its domestic competitors, most of which are large, diversified chemical companies.

ASIX’s products are derived from the chemical chains illustrated in the graphic below.

Source: AdvanSix 2024 10-K.

Nylon 6 is used to make fibers for textiles, automotive parts, carpets, clothing, and engineering plastics such as gears and bearings. Its strength and heat resistance make it an effective electrical insulator, while its durability makes it suitable for packaging.

Caprolactam is the key feedstock to nylon 6. ASIX is the global low-cost caprolactam producer, which confers a durable competitive advantage as long as end markets are not glutted, as they are today. The caprolactam market is consolidated, with the top three producers, Fibrant, BASF, and Sinopec, holding more than 30% market share.

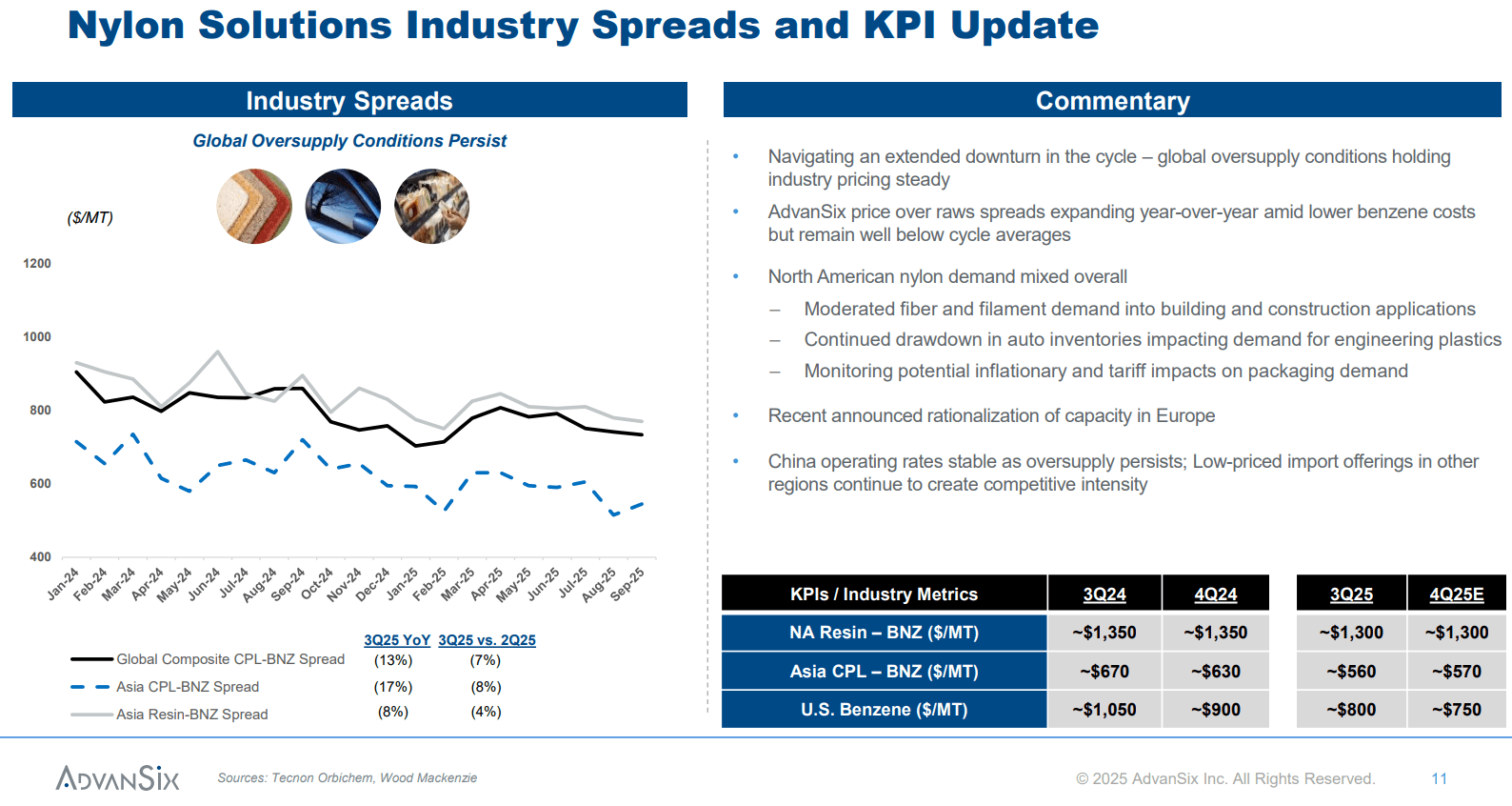

As in other chemical segments, global supply capacity for nylon 6 and caprolactam has expanded significantly in recent years, with China leading the charge. At the same time, global demand has been weak. The combination of rising supply and tepid demand led to price declines. Low prices for both caprolactam and nylon 6 have driven margins and capacity utilization lower since 2023. ASIX provided the following data on the nylon market in its third-quarter earnings call presentation.

Source: AdvanSix Q3 2025 Earnings Presentation, Nov. 7, 2025.

The removal of high-cost supply will drive an initial recovery. The recovery will progress as capacity utilization rates increase.

The outlook is more constructive over the longer term. Nylon 6 and caprolactam are expected to grow at a mid-single-digit rate through the early 2030s, driven by higher demand for auto parts, plastics, electronics, and textiles.

Ammonium Sulfate

The Raschig process by which ASIX produces nylon 6 throws off significant volumes of ammonium sulfate, which the company sells as fertilizer. Ammonium sulfate is nitrogen-rich, providing plants with the nitrogen and sulfur they need to grow.

Ammonium sulfate’s near-term outlook is brighter than nylon’s, as end markets are not glutted. Ammonium sulfate is also expected to grow in the mid-single-digit percentage range over the coming years, driven by higher demand from agriculture. Agricultural demand from year to year depends on crop prices and planting intensity.

Sulfate demand has remained robust even in recent quarters. ASIX is currently transitioning its product toward “granular ammonium sulfate,” which is easier to spread, slower-releasing, and has higher sulfur content than common substitutes. Due to its various benefits, the granular product is sold at a premium.

By the end of 2025, ASIX will have transitioned 72% of its ammonium sulfate production into higher-margin granular form. The company has dubbed the transition to granular its “SUSTAIN” program. The program is aimed at increasing the company’s granular ammonium sulfate capacity by 200,000 tons, which fetches a premium of $75 per ton. The premium stands to increase ASIX’s mid-cycle Adjusted EBITDA by more than $15 million annually.

ASIX’s SUSTAIN program has consumed most of its growth capex in recent years. The project is slated for completion in 2026, and capex should decline in 2027 and beyond.

Chemical Intermediates

In addition to ammonium sulfate, ASIX’s nylon 6 manufacturing process throws off various chemical intermediates that the company also sells. These products include phenol, acetone, and other co-products. Growth from these chemical intermediates is expected to track in the low single digits over the coming years.

ASIX benefits from structurally higher acetone prices and margins attributable to U.S. antidumping tariffs. Imports have declined from 230,000 tons in 2018 to 64,000 tons in 2024, driving acetone-propylene spreads from $0.10 per pound to a sustainable range of $0.15 to $0.20 per pound. The larger spread stands to add approximately $30 million to ASIX’s mid-cycle Adjusted EBITDA.