How To Navigate The Incoming Oil Price Weakness

By: Jon Costello

Barring some unforeseen geopolitical shock, oil prices are heading lower.

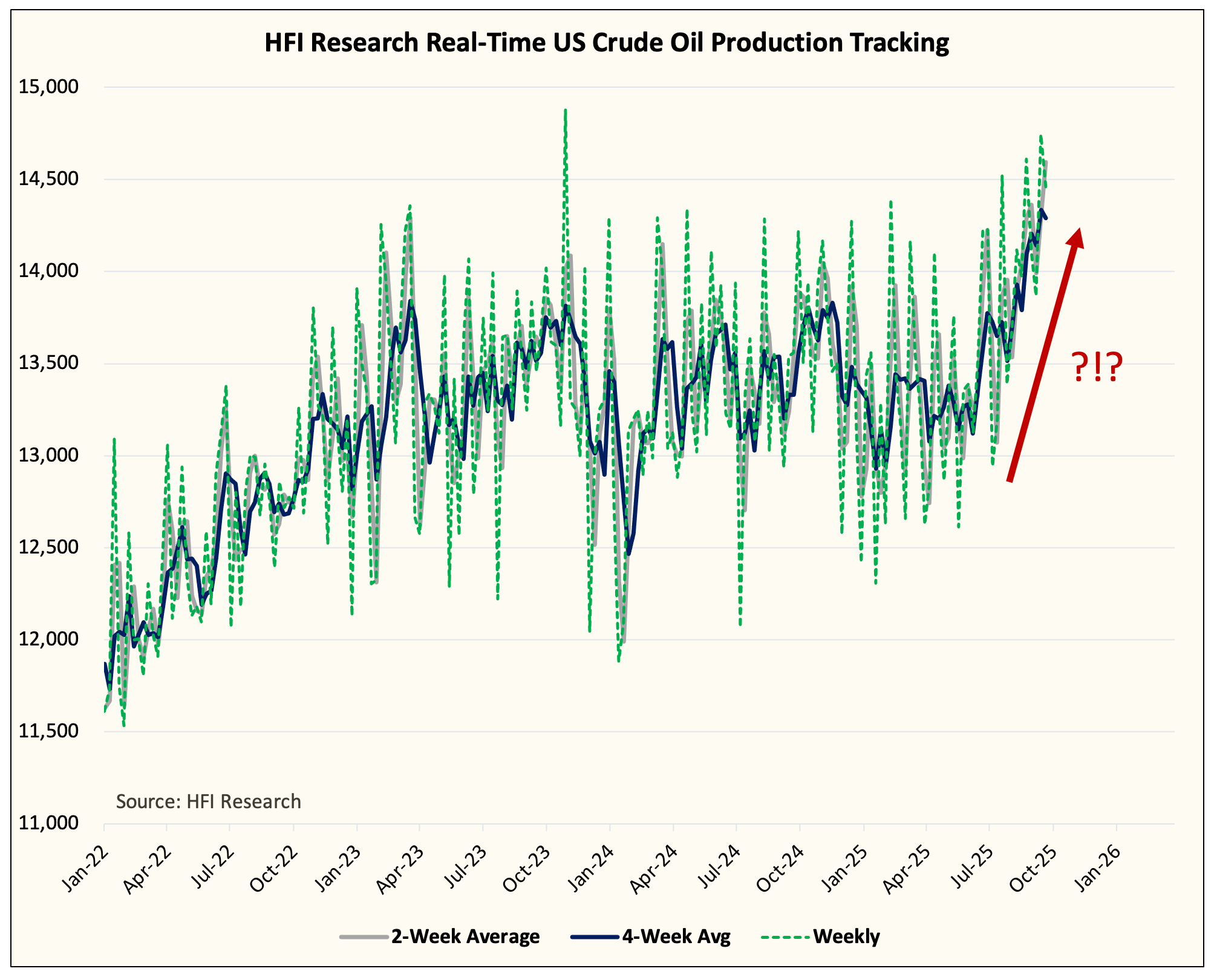

Supply is surging. US production is significantly outperforming virtually all forecasts made at the beginning of the year.

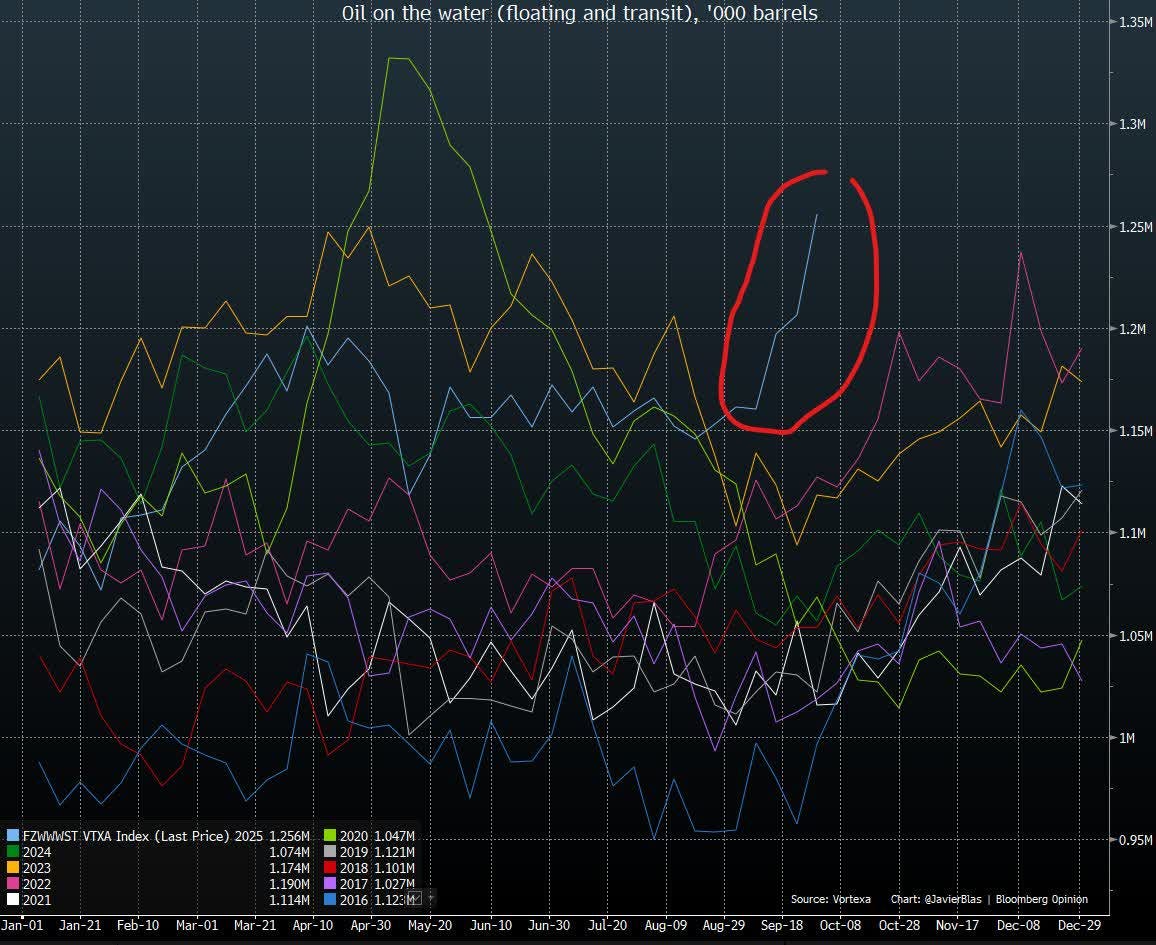

Meanwhile, an armada of tankers is departing OPEC and is set to arrive at global ports during peak refinery maintenance season.

Source: Javier Blas, X, Oct. 2, 2025.

Rising crude oil inventories will cause the physical market to deteriorate over the coming weeks and months, sending prices lower. Clearly, this is a time when investors should tread cautiously in allocating new funds to the energy sector.

Oil prices already discount the impending oversupply. WTI has remained well below $70 per barrel because the oversupply has been widely expected. The market’s consensus setters, such as the IEA and sell-side analysts, have publicized it relentlessly all year.

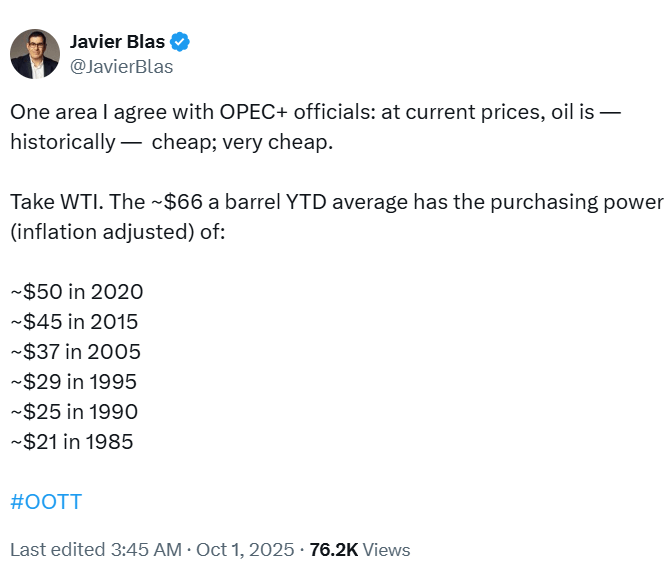

One way to better appreciate today’s low oil prices is to adjust them for inflation.

Source: Javier Blas, X, Oct. 1, 2025.

I’ve lived through the 2020 and 2015 episodes—and the 2009 low, which is not listed above—as a professional investor. In 2020, we had the Covid downturn; in 2015, glutted oil markets sent prices to a cyclical low in the $20s; back in 2009, the financial world and economy were in crisis.

Given the state of the oil market during those past episodes and the pervasive fear that gripped investors, the fact that current prices are anywhere near those levels in a market that has yet to experience an oversupply is amazing.

The charts below show what price today’s $61 per barrel WTI would be at the trough of those bear markets when adjusted for inflation. The figures are calculated from the Bureau of Labor Statistics’ CPI inflation calculator. The figures drive home just how low current prices are.

Oil prices are low based on other metrics, as well. For example, the price of an oil barrel is depressed compared to almost any other major commodity based on historical price correlations.