Here Are Three Names To Buy As Trump's Canadian Tariff Threat Looms

By: Jon Costello

Note: Dollar values are in Canadian dollars unless otherwise specified.

Earlier this week, we discussed how investors are selling Canadian stocks first and asking questions later about Canadian energy stocks. The selling has created attractive long-term investment opportunities in the Canadian E&P space.

Since tariffs have been discussed, Canadian E&Ps have sold off relative to energy commodities and their U.S. peers. The following chart shows the relative performance of WTI, Canadian E&Ps (XEG:CA), and U.S. E&Ps (XOP) since the U.S. election.

The XEG ETF has underperformed WTI by 11.8% and the XOP ETF by 10.3% since late October, indicating the potential for a nice rally if the tame tariff scenarios we expect actually play out.

The current setup among Canadian E&Ps represents an opportunity because the worst-case scenario of a 25% tariff on Canadian energy exports is extremely unlikely. Even if tariffs are imposed, their impact will be muted and short-lived. Consequently, the financial impact on our favorite names won’t be as severe as implied by their recent price action.

Impact on E&Ps Less Severe than the Market Expects

We don’t believe President-elect Trump wants to place tariffs on Canada. He’s using them as a tool to force Canadian politicians to the negotiating table. In the end, tariffs are in no one’s interest. They would hurt both Canada and the U.S. economies while souring an extremely important trading partner for both countries.

Signs have already emerged that the 25% tariffs that Trump has threatened will not be imposed all at once. Trump’s cabinet nominees are already considering applying tariffs incrementally. The proposals raise the tariff rate by 2% to 5% per month, as opposed to a 25% tariff imposed at once.

This approach would make sense. As the adverse impacts of the tariffs on the Canadian economy increase at a gradual rate, they will increase the pressure on Canadian politicians to act without severely damaging the Canadian economy. Canada’s economy is weak, so it would quickly feel some impact from even 2% tariffs. Canadian politicians looking to remain in power would be more likely to accede to Trump’s demands before the tariffs inflicted significant damage on the economy. We would expect politicians to buckle to Trump’s demands well before the tariffs reach their full 25%.

By the time the Canadian federal election takes place on or before October 20, the new Prime Minister—presumably Pierre Poilievre—will have little choice but to deal with Trump.

Higher Heavy Oil Prices Will Offset the Impact of Tariffs

Canada has the means to retaliate against the U.S. and protect its domestic energy industry. Canada’s provincial leaders have discussed retaliatory moves that include more than US$100 billion of tariffs on Canadian exports to the U.S. Presumptive future Canadian prime minister Pierre Poilievre has hinted at export tariffs on Canadian oil specifically, as well as the possibility of building more pipelines to the Canadian West Coast to reduce reliance on the U.S.

Higher heavy crude oil prices would get an additional boost relative to other crude grades if Alberta curtailed its local oil production, most of which gets exported to refineries and trading hubs in the U.S. There is precedent for curtailments. Alberta most recently curtailed production by more than 300,000 bbl/d in 2019 and 2020 in response to a regional glut.

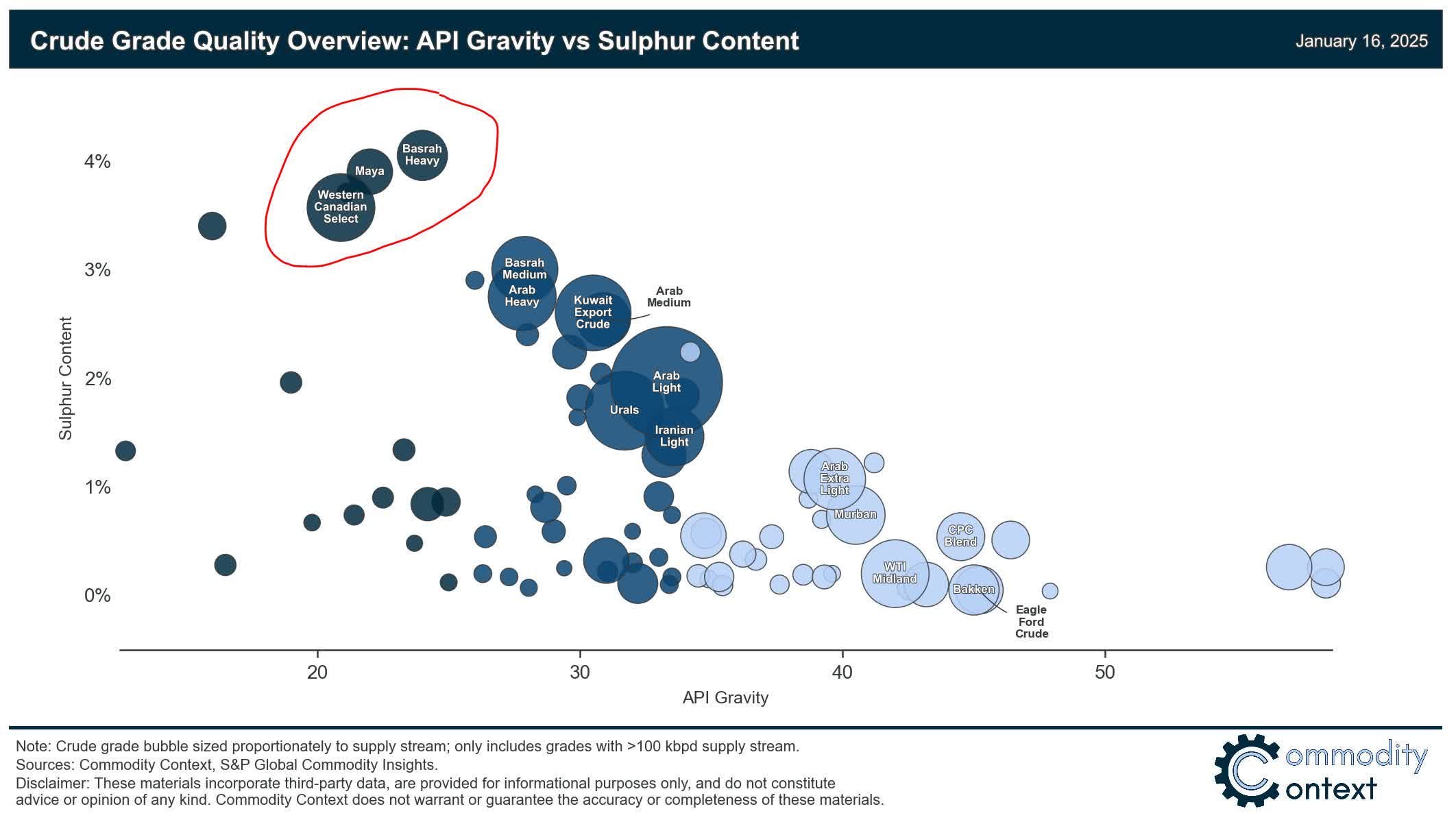

Alberta production curtailments would represent an effective way to counter the tariff impact on the Canadian energy industry, as they would reduce the WTI-WCS differential. Alternatives to Canadian heavy oil aren’t available to U.S. refiners that depend on them, creating a degree of price inelasticity for heavy oil purchases. Canada is the largest global producer of heavy oil, with few available replacement grades, as illustrated in the chart below.

Source: Rory Johnston, X, Jan. 16, 2025. The chart is not meant to be exhaustive, though it covers the major global crude grades.

If Alberta curtailed production volumes, U.S. heavy oil inventories would get worked down while replacement barrels wouldn’t be readily available. Refineries will be forced to bid for scarce heavy oil barrels.

Higher heavy oil prices from tariffs and heavy oil production curtailments would bolster the financials of Canadian E&Ps. At the same time, they would increase prices for U.S. refined products. The impact would be initially seen in the U.S. Midwest, an important electoral region for Trump. Eventually, it would spread throughout the rest of the country, creating a headache for consumer sentiment and electoral prospects for Trump-affiliated politicians.